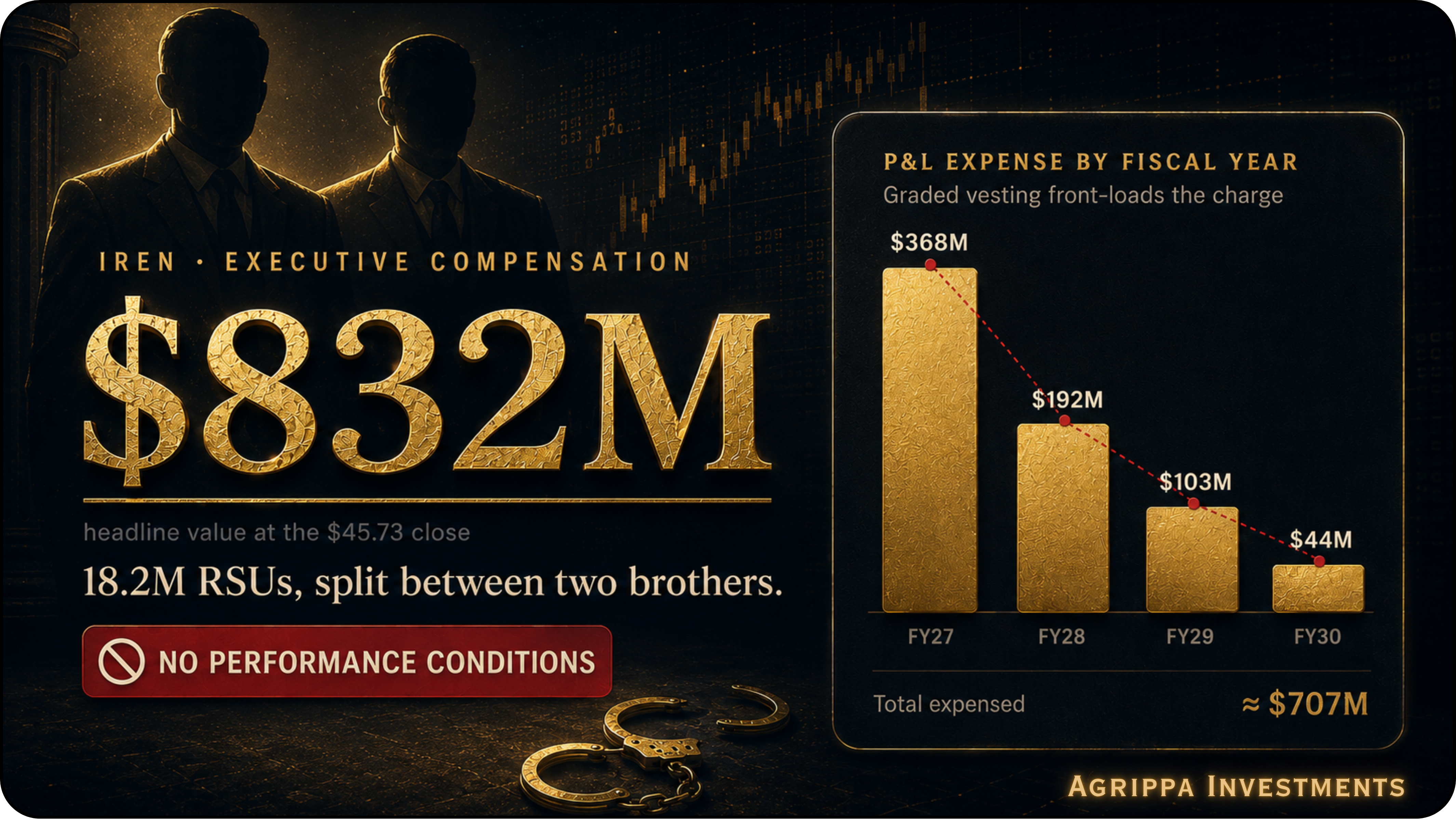

On June 30, IREN’s board approved what is by far the largest compensation decision in the company’s history, granting each of the two Co-CEOs 9,099,328 restricted stock units, or roughly $832 million combined at the share price on the day of approval. The award vests in four equal annual installments over the coming four years, each vested tranche carries an additional two-year holding period, and neither brother will receive another equity grant until fiscal year 2031. Within hours of the 8-K hitting the wire, my inbox and timelines made it very clear that this would become the most controversial thing IREN has done as a public company.

Investor sentiment has taken a serious hit since. Virtually every seed investor I'm in contact with is at the very least disappointed, and many of the larger retail holders I speak with regularly have been openly critical of the package. The anger is real, it’s broad, and I don’t think it can be waved away as noise from people who don’t understand how founder compensation works. So before getting into the mechanics of the package itself, it’s worth understanding why the reaction has been this intense, because in my view it comes down to two factors compounding each other.

The first is that this lands on an investor base that was already frustrated. IREN’s share price has heavily underperformed its peer group over the past six to eight months. The most direct comparison is Nebius, which scaled its topline beautifully over the past twelve months, signed a series of high profile deals, and watched its stock get rewarded handsomely for it. The picture doesn’t improve much when you compare against IREN’s former Bitcoin mining rivals that followed it into the data center space. Names like Cipher, Hut 8, Applied Digital, and Core Scientific are all up substantially on IREN over the past two to four quarters, depending on the ticker and the window you choose. What makes this sting so much for longtime holders is that IREN entered this transition with a materially stronger hand than pretty much all of them, holding multiple mega-sites and multi-gigawatts of grid-connected power while most of the mining cohort was still assembling its first serious campus. Yet IREN is the one whose share price is lagging. Layered on top of that is a cohort of investors who bought IREN primarily to ride the AI infrastructure wave for a year or two, and who are now realizing that, at least over the past six months, they picked the wrong horse for that particular trade. The mix of genuine long-term disappointment and frustrated momentum money has produced an environment where everything IREN does gets scrutinized harder and amplified louder than it would in calmer times. Patience was already thin before this 8-K existed.

The second factor is the package itself, which is genuinely enormous by any benchmark you care to apply. Since IREN runs a co-CEO structure while convention is a single chief executive, I think the honest way to size it is the combined figure, because that’s what the company is paying for the CEO function as a whole. At roughly $832 million over four years, the two brothers together will earn more per year than Satya Nadella receives for running Microsoft, more than Tim Cook receives for running Apple, and multiples of what Sundar Pichai averages at Google outside his periodic mega-grant years. Each of those men runs a company worth one to four trillion dollars. IREN is a fraction of one percent of that scale and is not yet even a member of the S&P 500, an index in which this package would rank among the ten largest compensation arrangements outright.

And size, on its own, still isn’t the core of the complaint. The past year produced a wave of even larger founder packages, from Elon Musk's new Tesla arrangement, carrying a grant value north of $130 billion, to Broadcom potentially paying Hock Tan over $200 million and Wayfair granting Niraj Shah performance stock units currently valued at $280 million. What separates every single one of those from the IREN grant is that they are earned against something. Tan forfeits his entire award if Broadcom’s AI revenue falls short of defined targets. Shah’s shares only vest if Wayfair’s stock reaches price hurdles set between two and nearly seven times the level at grant. Musk's package is structured around Tesla's market value climbing in enormous steps alongside operational milestones, and pays nothing on any tranche whose targets aren't reached. The Roberts brothers’ package has none of that. The 18.2 million RSUs vest in full as long as the two of them remain employed through each annual vesting date. The two-year holding periods do add something, since each tranche stays locked from sale for two additional years after vesting, but a restriction on when you can cash out is a very different thing from a condition on whether you earn the shares at all. Reduced to its essence, showing up to the office for four more years is the entire performance requirement.

Take those two angles together, a frustrated shareholder base primed to assume the worst and a package whose structure is objectively out of step with every comparable mega-grant of this cycle, and the intensity of the uproar makes complete sense.

What I want to do in this piece is give you my honest perspective on it, working through what this package actually costs IREN over the coming years, a few angles I believe the public discussion has missed entirely, the governance questions it raises, and most importantly, whether any of this changes the investment thesis. Some of what follows will validate the criticism, and some of it will push back against it. By the end you should have the full 360 degree picture.

Is this a thesis breaker?

I think it’s well suited to start with the most important question of all, which is whether this package breaks my long-term thesis on IREN. Everything else in this piece, the governance debate, the question of fairness, the shareholder response, sits downstream of that answer. And to answer it properly, we have to work through a few variables and assumptions, the first being the actual financial impact of these RSUs over the coming years.

For context, my thesis on IREN was never just that the company becomes the next hyperscaler and the category leader among neo-clouds. It’s that earnings power ultimately drives the valuation and the value creation forward. I have no interest in owning a high growth story with no realistic path to real GAAP net income. The whole point of IREN’s vertical integration on the infrastructure side is not just that it enables more control and faster growth, but that those advantages compound into a highly profitable cloud business at scale. That's the lens through which this package has to be judged as far as the thesis question is concerned. Nearly 20 million new shares are being handed to the two founders, those shares have to be accounted for, and stock-based compensation is a very real expense on the GAAP income statement. So the fair question is how badly this dents the earnings trajectory the thesis depends on.

Now, some of you might assume these costs are variable, meaning the higher the share price climbs over the coming years, the more this package degrades profitability. Under that logic, if IREN ends up trading at $200, the roughly 4.5 million shares vesting that year would suddenly represent $900 million of compensation expense, wrecking the bottom line right as the business hits its stride. It feels intuitive, and I’ve seen versions of this argument circulating since the 8-K dropped. Luckily for shareholders, that is not how the accounting works.

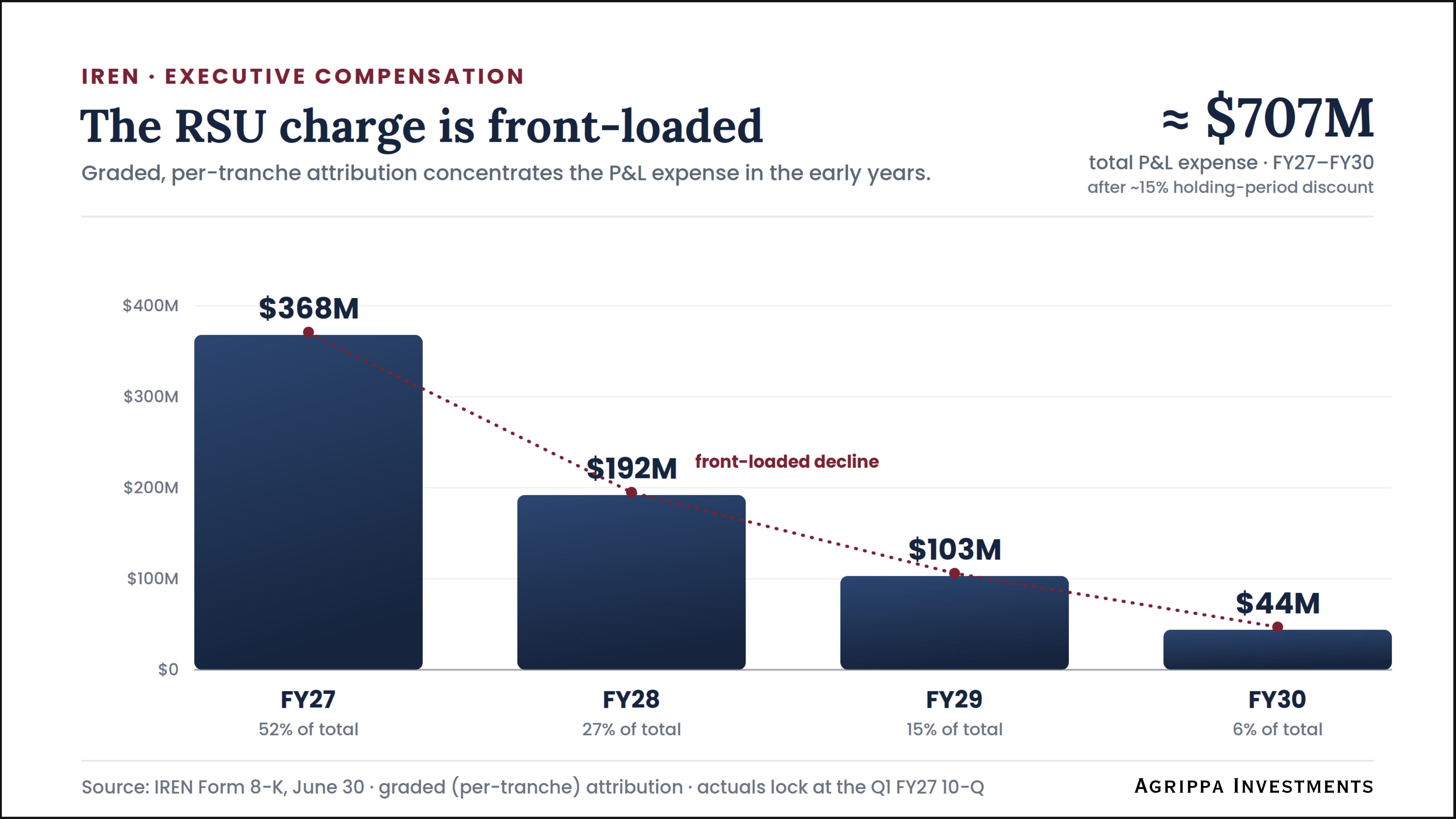

Under US accounting rules, an RSU award is valued once, on the day it’s granted, and that value never changes afterwards. The measurement is essentially the share price at grant multiplied by the number of units, which puts the headline figure at circa $832 million based on the $45.73 close on June 30. Whether the stock trades at $200 or at $20 when the shares actually vest is irrelevant to the income statement. The upside beyond the grant price never touches the P&L, and neither does the downside. On top of that, the recognized figure will land somewhat below the headline number, because the accounting framework allows a mechanical discount for the two-year sale restriction attached to each tranche. The logic is that a share you’re barred from selling for two years is worth less than a freely tradable one, and for a stock as volatile as IREN that discount typically runs somewhere in the 10 to 25 percent range. Using a middle-of-the-road 15 percent, the amount that actually flows through the P&L comes out around $700 million spread across four years. The precise figure will be confirmed in the first quarterly filing of fiscal 2027, so treat my numbers as close estimates until then.

The spread across those four years is where it gets more interesting. Companies can recognize this kind of expense in equal annual amounts, or through what’s called the graded method, which treats each annual tranche as its own award and expenses it over its own vesting window. IREN’s filings show the company uses the graded approach, and the practical consequence is heavy front-loading. Roughly 52% of the entire package hits the P&L in fiscal 2027, about 27% in fiscal 2028, around 15% in fiscal 2029, and just over 6% in fiscal 2030. As you can see in the graphic below, that’s approximately $368 million this fiscal year, $192 million next, then $103 million, then a final $44 million.

So the sting is concentrated almost entirely in the four quarters we just entered, and it fades fast from there. That shape happens to align remarkably well with how I expect IREN’s earnings to ramp anyway. Fiscal 2027 was always going to be a suppressed year on the bottom line, weighed down by the aggressive headcount growth and the SG&A buildout that comes with scaling into a serious cloud brand. Those costs are largely fixed in nature, they don’t scale linearly with revenue, and as revenue pushes toward the double digit billions over the coming two years, operating leverage does the heavy lifting on profitability. By fiscal 2029 and 2030, precisely the years in which I expect IREN’s earnings power to properly show itself, this package is down to a $103 million and then a $44 million line item. Against the earnings base I’ll get to in a moment, that’s a rounding error.

This is also where I want to directly address the timing anger, because it’s one of the most common complaints I’ve seen. The argument goes that the board should have waited, that a package like this should be granted after major milestones like the Horizon buildout are delivered, once the stock is much higher and shareholders have actually been paid. Dropping this 8-K into the depths of negative sentiment, with the share price already underperforming the peer group, feels tone deaf at best. I understand that reaction, and from a pure investor relations standpoint the timing genuinely is terrible. But here’s the uncomfortable trade-off embedded in that complaint. The size of the P&L hit is set by the share price on the grant date. Had the board waited for the stock to triple before granting the exact same number of shares, the expense flowing through the income statement over the following four years would have tripled with it. A package this size granted at $120 or higher would be dragging well over $2 billion through the P&L instead of ~$700 million, weighing on every single year of the earnings ramp the thesis depends on. You simply can’t have it both ways. Either the grant lands when sentiment is low and the accounting cost is low, or it lands after the celebration and costs multiple times as much on paper. Purely from the perspective of IREN’s future income statement, the depressed share price is a blessing in disguise, however unsatisfying that feels emotionally.

The second variable is dilution, and here I won’t sugarcoat the raw number. Against the roughly 360 million shares outstanding in the most recent filing, 18.2 million new shares represent about 5 percent of the company being transferred to the two founders. Taken in isolation, that’s a lot. But dilution at IREN can’t be judged in isolation, because this remains a company investing enormously into its infrastructure buildout, and equity will keep being raised to fund it for a while yet. I’ve made the case in multiple deep dives here on Substack that the need for equity issuance should materially diminish over time, as IREN builds a flywheel of reinvesting its own operating cash flow into the buildout while layering asset-backed financing onto stabilized, revenue-generating sites. I still firmly believe that. But the honest reality is that the share count will keep growing substantially over the coming 18 to 36 months regardless, and investors should set their expectations accordingly. My own working assumption is that the count can grow toward 500 to 600 million shares by 2030. Against ~250 million potential new shares hitting the market as the company scales, the 18.2 million from this package is closer to a drop in the bucket than a structural break. I was, in effect, already underwriting dilution of this magnitude before the 8-K existed, and the package doesn’t materially change that picture.

What matters is what shareholders get in exchange for carrying that dilution. By 2030 I expect IREN’s operational data center footprint to reach at minimum around 3 GW gross, translating into roughly 2 GW of IT capacity, and quite possibly more. Take the economics of the recent 60 MW NVIDIA cloud deal, which I have analyzed to death in our recent IREN deep dive, and discount them heavily, and IREN should still be earning at the very least about $3 million per IT megawatt per year (pre-tax) on that infrastructure. That figure is on a project level basis, meaning it already absorbs all financing costs, data center depreciation, a five year GPU depreciation schedule, and the operating expenses of actually running the clusters, from energy to personnel. It could also prove multiples higher depending on how large the share of high yielding enterprise customers becomes within the total customer mix. On 2 GW of IT capacity, that conservative per-megawatt figure produces roughly $6 billion of pre-tax project level earnings. Deduct corporate overhead, which even at the very top end I’d size at $500 to 800 million per year, inclusive of the founders’ package at that point, and you’re comfortably left with over $4 billion of net income after tax.

Apply a 75 times earnings multiple to that, which I consider defensible for a company still compounding earnings at well over 100 percent per year at that stage, and you arrive at a valuation of around $300 billion. Even against a fully diluted future count of 600 million shares, that’s a share price of $500. If you think my multiple is too generous, fine, cut it in half, and you’re still looking at $250 per share, more than a 5x from today’s levels within a handful of years. And keep in mind where I’ve been conservative. The footprint assumption is a floor, the per-megawatt economics are heavily discounted from the NVIDIA deal’s actual terms, meaning earnings by 2030 could plausibly land well above $10 billion, which would push the valuation dramatically higher. Meanwhile my share count assumption is deliberately aggressive, and if issuance comes in at 150 or 200 million new shares instead of ~250 million, the per-share picture improves further still.

So the bottom line, at least for me, is that this package is immaterial to the long-term thesis. The P&L drag is front-loaded into a year that was going to be earnings-suppressed anyway, it decays to insignificance exactly as the earnings ramp arrives, and the dilution disappears into a share count trajectory I had already underwritten. That said, these are my estimates, built from my own modeling and industry research. If your assumptions are meaningfully more pessimistic than mine on the buildout pace, the unit economics, or the customer mix, then I fully acknowledge that both the dilution and the P&L hit from this package could tilt your version of the thesis in a way it doesn’t tilt mine. I can only speak for my own framework, and within it, having done the level of due diligence I’ve done on this company, the conclusion is clear. The upside for shareholders remains enormous if the company delivers on its ambitions, and this package doesn’t change that.

The Governance Angle

Let me start with what I consider the most preventable part of this entire situation, which is the absence of any milestones. From all the conversations I’ve had since the 8-K dropped, I’m convinced that a good portion of investors would have accepted the sheer size of this package without much protest if the tranches had simply been tied to something. Business KPIs, operational targets, share price hurdles, anything that establishes the basic sequence of you do the work, shareholders benefit, and then you get paid. Simple and fair. It’s also the structure IREN itself has used before. The founders’ previous awards were largely built around share price milestones requiring the stock to multiply several times over before anything vested, and I was a big fan of how that previous package was originally designed. This one has none of that. The RSUs vest on time alone, and the only thing the founders are accountable to is their own continued employment. If they created zero shareholder value over the next four years and the stock went nowhere, they would still collectively walk away with over $800 million worth of stock at the grant date price. However you feel about the brothers and their track record, that asymmetry is plainly unfair to the people funding it, and I was firmly in this camp from the moment the filing hit, voicing the need for milestones publicly ever since.

A recent comment from Andreas Knopf on our subscriber Discord made me soften my stance on this topic, and his theory has since gathered real traction as people began sharing it on X. The short version goes like this: The founders’ B Class shares, which carry their outsized voting power, expire in 2033, which happens to be the exact year the final tranche of this package unlocks. Under his reading, the grant is less a monetary reward and more a way of locking in as much voting weight as possible before that privilege disappears, and that’s precisely why the tranches are unconditional. Shares that might not arrive because a milestone gets missed are useless as a control instrument, so the founders were never going to accept conditions on them.

That theory made me reconsider my stance, though I don’t think it’s only about life after 2033. I think it’s just as much about the years leading up to it. To understand where I’m coming from, you first need to see how IREN’s voting power is actually structured. Each brother holds one B Class share, a special instrument that grants its holders 15 votes for every ordinary share they own, while every other shareholder gets the standard one vote per share. The consequence is that the founders’ true voting weight is a multiple of their economic stake. Based on the most recent filings, the two of them together hold somewhere around 28 million issued shares, under 8% of the company economically, yet through the multiplier that translates into roughly 56% of all votes by my estimate. That is firm control. On any matter put to shareholders, from board composition to strategic direction, nobody can outvote the Co-CEOs. But that control does not stand still. Every share issued through the ATM program and every acquisition paid in stock adds votes to everyone else’s side of the ledger while theirs stays fixed, so the founders’ grip erodes mechanically as the company keeps raising equity to fund the buildout. The RSU package counters exactly that. Each vesting tranche adds millions of ordinary shares to their holdings, and each of those shares carries 15 votes for as long as the B Class instruments live.

I’m quite sure the founders would do a lot to preserve that control, especially with shareholder opposition as loud as it currently is. It’s evident to anyone who follows the company closely that the brothers hold their cards extremely close to the chest. From an investor relations perspective that approach is a nightmare, but competitively it has obvious advantages, and it produces a recurring pattern I’ve watched play out several times now. Shareholders strongly oppose something the company is doing or not doing, only to do a complete 180 once the fuller picture emerges. Horizon 1 is the cleanest example. Early last year, when IREN started building an expensive AI purposed data center without a signed lease in place, a large part of the shareholder base considered it reckless, and the criticism was loud. Only later did it become clear that starting the build early was what allowed IREN to secure Microsoft as a cloud tenant, since the capacity actually existed on the timeline the customer needed. There have been plenty of moments like that, and the intensity of the opposition has usually tracked wherever the share price happened to be trading at the time. Seen from the founders’ chairs, heading into the most critical and transformational phase in the company’s history, I can understand the desire for absolute control over the ship. Every founder of this generation knows the story of Steve Jobs, who got pushed out of his own company by his own board. And I’ll say openly that as a shareholder I actually want these two steering IREN for as long as possible. Generally speaking, I favor investing in founder led businesses whose leaders sit firmly in control, with little risk of some activist group forcing its way onto the cap table and ruining the party. That preference applies here as much as anywhere.

Their trading history supports the control reading too. Since the IPO, the brothers have never sold shares except on two occasions, and both had the fingerprints of tax events all over them. Each time, the sales coincided with legacy stock options approaching their expiry date, which forced an exercise. Under Australian tax law, exercising options creates an immediate income tax liability on the full gain at rates approaching half, and unlike in the US there is no automatic withholding mechanism that handles it for you, so selling a portion of the position is essentially the only way to fund the bill. Roughly a million shares each, in amounts that map closely onto what those tax obligations would have required. Beyond those two forced episodes, not a single share has left their hands in five years as public company executives. The two year lock-up on each tranche of the new package fits neatly into the same picture, since the structure plausibly defers the Australian taxing point on each tranche until its restriction lifts, meaning no forced selling at any vesting date and every vested share staying in their hands, voting, for at least two additional years. So all of that said, I think this angle deserves genuine consideration. It doesn't automatically make the package fair or justified, but it paints a more nuanced picture, one that isn't just about the monetary value alone.

However, none of this makes the governance questions go away, and this is where my sympathy ends. Because there’s a part of this story that most investors have missed entirely, and it changes how the whole situation should be read. The milestone based package I praised earlier, the one requiring the stock to multiply before anything vested, did not actually run its course. In May 2025, with the share price sitting near its local lows, the board amended a large portion of those awards and stripped the performance conditions out entirely, converting them to simple time based vesting. The board’s reasoning was that despite IREN’s strong operational performance, the retentive value of the awards had been significantly diminished by market wide structural factors and macro volatility. And to be fair, I don’t consider that reasoning absurd on its face. The macro backdrop at the time was genuinely awful, and even great companies watched their stocks get crushed on nothing but market fears.

What I take issue with is the principle. That package was designed the way it was designed, both sides knew the terms, and the milestones existed precisely to tie the founders’ payday to outcomes shareholders actually feel. The moment it looked like those shareholder aligned targets might slip out of reach, the board went back on its own word and rewrote the deal to save the package. Whatever the surrounding circumstances, that is back-pedaling on an agreed contract the instant it threatens to bite, and it tells you what this board is actually there to do. As it turned out, the stock more than tripled in the months that followed, meaning the original milestones would in all likelihood have been hit anyway, and the founders collected through time based vesting what they were probably about to earn on merit. So the current package is not the sudden departure many investors believe it to be. It’s the second consecutive move in the same direction. If the control theory is right, I can even understand why locking in those shares mattered so much to the founders that they pushed for it. But understanding the founders' motive does nothing to excuse the board, whose entire purpose is to hold the line in situations like these.

And that brings me to the board itself, because in my view this is where the real structural problem sits. IREN's board is still largely the board of the Bitcoin mining era. It's small, it has seen no meaningful additions since the company pivoted into AI infrastructure, and it consists largely of people whose track records have little application to the direction IREN is heading. What the next chapter actually demands are directors with backgrounds in hyperscale data centers, enterprise cloud, large cap capital markets, and the kind of compensation governance that companies of the size IREN wants to become take for granted.

I want to be careful and fair here, since this same board oversaw one of the most successful corporate transformations in the market, and outcomes count for something. But the pattern of the last eighteen months, a short term bonus paid at maximum, performance conditions amended away near the lows, and now the largest unconditional grant of this entire compensation cycle, all approved unanimously, points to a board that reviews what the founders want and finds ways to say yes. With voting control mathematically beyond challenge, board quality is the only real oversight IREN shareholders have left, which is precisely why it needs to be stronger than this. I support founder control, but supporting founder control while asking for a serious board refresh is not a contradiction. As IREN scales its operating footprint deep into the gigawatts and positions itself among the most important AI infrastructure companies in the world, the maturity of its boardroom should scale with it, and right now it visibly hasn't.

Justified or not?

With the mechanics, the thesis impact, and the governance picture covered, what’s left is the judgement call, and to make it honestly I want to work through the two real questions at the center of this debate. Whether the founders are actually aligned with shareholders, and whether the milestone based alternative everyone is demanding would truly have served shareholders better.

On alignment, let’s start by conceding the criticism in full. The founders get rewarded no matter what they deliver. Even if the share price halved over the vesting period, each brother would still collect roughly $200 million worth of stock over the six year span of this structure, an extraordinary amount by any measure, and one they receive simply for staying in their roles. That is the reality of the package, and no amount of framing changes it. But it's worth being precise about what exactly the problem is here. The guaranteed payout is a fairness problem, no question. Whether it's also an alignment problem is a separate matter entirely, and I'd argue it mostly isn't.

As previously pointed out, in five years as public company executives, the brothers have sold shares exactly twice, and both episodes carried the clear fingerprints of forced tax events tied to expiring options. Outside of those, not a single share has left their hands through the entire journey from a multi-hundred million dollar Bitcoin miner to where IREN stands today. Founders who don’t believe in the long term trajectory of their company typically don’t behave this way. Then layer on the structure of the package itself. Because of the two year lock-up trailing each tranche, the earliest moment they can sell even the first slice of this award is three years from now, and the final tranche stays untouchable until 2032. If they ever intend to monetize this equity, whether by selling it outright or by collateralizing it for financing the way many founders prefer, the share price at those future dates is what determines what it’s all worth.

And then there’s an angle that may sound ridiculous on the surface but paints a surprisingly clear picture. The Roberts brothers, Dan in particular, seem to carry the ambition of becoming the richest people in Australia. I’ve now heard this from multiple people who know Dan personally, and while I can’t say whether he stated it to them directly or whether it’s their inference from knowing him, their assessment on this point has been firm. I’ll admit this cuts against the more charitable ‘control’ angle to some degree, since it suggests the monetary value itself is very much a big part of the picture. But notice what the ambition requires. Nobody becomes the richest person in Australia on a stack of locked up shares in a sideways stock. That goal is only reachable if IREN’s share price rises materially, and keeps rising, for years. However you weigh the motives, greed of that particular shape points in exactly the same direction as your portfolio does.

Now to the milestone question one final time, because from a fairness standpoint the case is airtight. You deliver, shareholders benefit, you get rewarded. I’ve argued for that principle publicly and I still consider it the right default. But from a pure incentive standpoint, the story is genuinely less clean than the public discussion assumes.

Suppose the board had attached this package to a set of business KPIs, whether ARR, contracted revenue, adjusted EBITDA, or any metric of your choosing. From that moment on, nearly a billion dollars of personal outcome is glued to a narrow set of deliverables, and leadership’s attention follows the money. Metrics outside the chosen set risk quiet neglect, and the overall long term health of the company can end up subordinated to maximizing whatever happens to be measured. Share price hurdles are better on this front, since the stock at least aggregates everything, but they aren’t perfect either. To force a stock through a defined level before a defined date, leadership can be nudged toward the quicker route, the one that plays best with investor sentiment in the short run. Think of favoring colocation deals over the cloud buildout because that’s what the investor base currently cheers for, or signing a shiny high profile contract that pops the stock but carries strings attached or is simply strategically inferior to alternative paths. None of this needs to be a persistent problem across the full four years to do damage. One such decision, made in the shadow of a tranche about to expire worthless, can bend the long term trajectory of a company permanently. So from a strict alignment perspective, I’d actually argue the current structure aligns the founders with long term shareholders better than a milestone linked alternative would, precisely because there is no artificial finish line distorting what they optimize for.

I want to be clear about the load bearing assumption underneath that argument. It only flies if you genuinely believe the founders have real ambitions to drive this company forward and to maximize their own wealth along with it. If your view is more cynical, if you think the founders fundamentally don’t care and would happily coast for four years collecting tranches, then fixed milestones were the only guardrail available. I understand that position. But everything I can observe points the other way. The founders can’t sell a single share of this award for the next three years, they’ve never voluntarily sold a share in five years as a public company, the personal ambitions run far beyond what this package alone could ever satisfy, and the sheer intensity with which they’ve carried this company from a small Sydney based startup to the doorstep of hyperscale is not the behavior of people planning to coast. Alignment, in my assessment, is not the issue here.

So to round off the judgement. No, I don’t think this package is fair, and I won’t pretend otherwise. But I do believe it’s in the best interest of shareholders. The founders are now locked into golden handcuffs for the coming four years, with their personal fortunes chained to the share price stretching well beyond that, in exactly the period where this company needs their full commitment the most. And while the timing of the announcement could hardly have been worse from an optics perspective, the depressed share price it was granted into quietly works in every shareholder’s favor a few years from now, given how much smaller the P&L drag will be relative to the alternative. Sometimes the version of events that feels worst in the moment is the one you’d have chosen with hindsight anyway.

That’s where I’ll leave this one. Thank you for reading through what became a much deeper rabbit hole than a compensation filing usually deserves, and I hope it gave you a nuanced picture.

Before you go, one announcement. Tomorrow we’re releasing our long awaited NUAI deep dive to all paid subscribers. It’s by far the most comprehensive report out there on this promising small cap data center play, and I’m confident it will live up to the high expectations. Stay tuned!

Read our last IREN Deep Dive here: IREN’s Path to Global Dominance

Disclaimer (NFA): This publication is for informational and educational purposes only — not investment, legal, tax, or accounting advice. Nothing herein constitutes a solicitation, recommendation, or offer to buy or sell any security or strategy. The author may hold — and may buy or sell without notice — securities, derivatives, or other instruments referenced. All opinions are the author’s, expressed in good faith as of publication, and subject to change without notice. Information is believed accurate but provided “as is,” without representations or warranties; errors or omissions may occur. Any forward-looking statements involve risks and uncertainties that may cause actual results to differ materially. Past performance is not indicative of future results. Do your own research (DYOR) and consult a qualified, licensed adviser who understands your circumstances before acting on this content. To the fullest extent permitted by law, the author and publication disclaim liability for any loss arising from reliance on this material.

Incentive comp should always be simple to understand and its motives clear. Ball is dropped here, and board got lazy. I’ve seen it many times. Doesn’t impact the thesis, but it’s not a good look and the board should’ve done a better job. This is incentive comp, not rewarding for the past.