Earlier this month, IREN held one of the most consequential earnings calls in the company’s history, reshaping the investment thesis to a major degree.

Not only did management secure a multi-layered partnership with none other than NVIDIA spanning the company’s 5 GW portfolio, but they also provided critical insights into the Mirantis and Nostrum acquisitions and global expansion ambitions.

In this deep dive I’ll cover the following topics:

Full breakdown of the NVIDIA partnership

Comprehensive analysis of the Mirantis and Nostrum acquisitions

Australia expansion

Operational Delays

Dilution: ATM usage and new convertible offering

Customer roadmap and near-term catalysts

Given the scale of what was just announced, this is one of the most important write ups we have published on IREN to date.

Enjoy.

The NVIDIA Partnership

By far the most important announcement of last week’s earnings release, and arguably of the company’s history, was the new NVIDIA partnership. The partnership is slated to span across IREN’s global 5 GW data center footprint, commencing at Childress in the form of a 60 MW cloud agreement.

The ramifications of this newly formed partnership couldn’t be overstated. It’s a one of a kind agreement with a lot of different moving elements and layers, all of which I’ll be exploring in this chapter.

IREN: An Extension of the NVIDIA Brand

The first thing to understand is that this partnership isn’t merely a one-sided, transactional arrangement where NVIDIA is the seller of hardware and IREN the customer. This partnership goes much deeper than that. IREN is now a consequential part of NVIDIA’s product launch strategy.

You might think I’m reaching, but the evidence is right in front of us. Going forward, IREN will deploy NVIDIA’s DSX architecture across its 5 GW portfolio and collaborate with NVIDIA to deploy DGX environments. To understand what that actually means, it helps to break down what DSX and DGX each are.

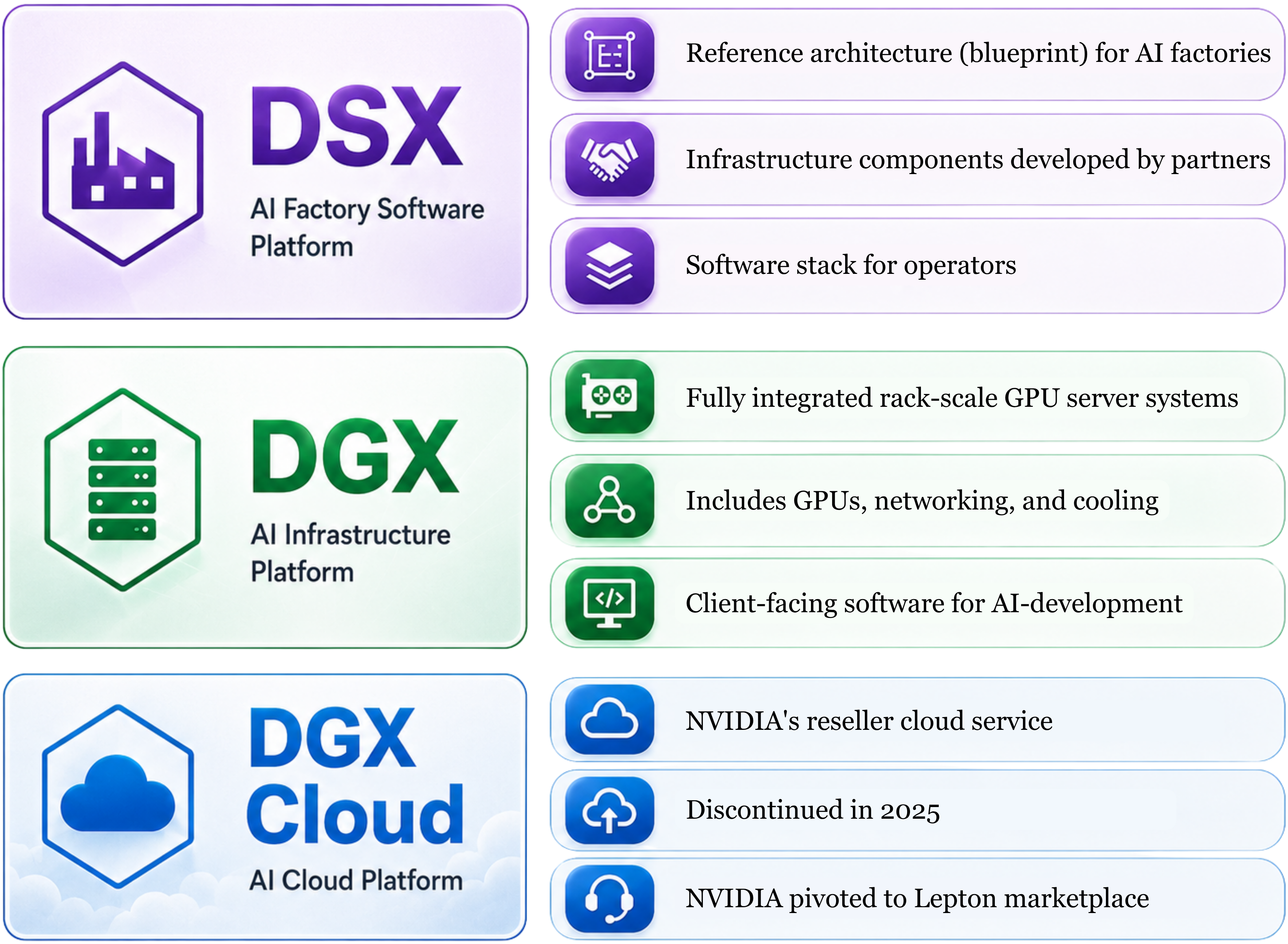

DSX

DSX is NVIDIA’s reference design framework for building and operating gigawatt-scale “AI factories”, a term Jensen Huang coined for modern AI data centers. It was first introduced by Jensen at GTC Washington D.C. in October 2025 as the Omniverse DSX Blueprint, and then expanded into the Vera Rubin DSX AI Factory reference design at GTC San Jose in March 2026, which adapted the framework specifically for the upcoming Vera Rubin chip generation.

DSX is not a product NVIDIA sells you in a box, but rather a reference design that defines how an AI data center should be built end-to-end, from the rack architecture and networking topology to the power distribution, liquid cooling, and grid integration. NVIDIA publishes the spec, and a broad partner ecosystem (Foxconn, Schneider Electric, Vertiv, Bechtel, Caterpillar, and many others) builds the actual physical infrastructure to that spec.

Every component of the DSX blueprint is designed to make NVIDIA’s compute products perform at a measurably higher level than they would in a generic data center. By co-designing the facility around the performance profile of NVIDIA’s hardware, DSX boosts efficiency and throughput across the board, which makes the underlying compute products more competitive and DSX the rational facility choice for any operator buying NVIDIA hardware at scale.

Alongside the physical hardware spec, DSX also includes a suite of operator-facing software. This software isn’t customer-facing, meaning end users leasing GPU capacity from a cloud provider like IREN never interact with it. Its purpose is to help the operator squeeze maximum performance out of its DSX-aligned infrastructure. This mirrors the logic on the hardware side. Every layer of DSX is engineered to extract more value out of NVIDIA’s underlying products.

The second strategic dimension of DSX is what it does to the upgrade cycle. AI hardware is evolving on a roughly annual cadence, with each new generation pushing higher density, higher power draw, and more demanding cooling requirements. For data center operators, that creates a serious problem. A facility built today for current-generation hardware could be technically obsolete within 18-24 months if it can’t accommodate next-generation deployments. Retrofitting a non-purpose-built facility for the next chip generation typically requires significant CapEx, prolonged downtime, and in some cases full demolition and rebuild.

A DSX-aligned facility avoids most of that pain. NVIDIA explicitly designs new chip generations with the existing DSX architecture in mind, ensuring the facility can accommodate upgrades with minimal modifications. The operator still incurs some costs at each generation transition, but the magnitude is dramatically lower than what a non-DSX facility would face, because the building, power, cooling, and control systems were designed against NVIDIA’s forward-looking specifications from day one.

The implication for NVIDIA is a quiet but durable form of ecosystem lock-in. Once an operator has built to the DSX spec, they’re structurally incentivized to continue deploying NVIDIA hardware because the facility is purpose-built for it and the upgrade path is dramatically easier than switching to alternative architectures. Migrating to custom hyperscaler ASICs or competing GPU vendors would require costly facility modifications that erase much of the original advantage. Yet for the operator, the trade-off is genuinely favorable. Future-proofing against rapid hardware evolution is one of the most expensive problems in the industry, and DSX largely solves it.

DGX

DGX is NVIDIA's branded turnkey AI server line. At its core, a DGX system is nothing more than NVIDIA GPUs (current generation B300s and soon-to-be Vera Rubin VR200s) wrapped inside a fully integrated server, complete with networking, storage, cooling, the customer-facing software stack (CUDA and related AI frameworks), and NVIDIA's enterprise support, all bundled into one product. You buy the box, plug it in, and you have a working AI compute system without having to source components and integrate them yourself.

The most common alternative path to deploying NVIDIA GPUs at scale is through Original Equipment Manufacturer (OEM) partners like Dell, Lenovo, or Supermicro. These companies use the same NVIDIA chips, but they handle the system integration themselves and sell the result under their own brand with their own support contracts. IREN’s historical procurement falls squarely in this camp. The ~76,000 Blackwell Ultra GPUs (GB300) procured for the Microsoft contract, for example, were sourced through Dell as integrated rack systems, not through NVIDIA as DGX-branded hardware.

The NVIDIA partnership could potentially shift this dynamic. Going forward, IREN may begin ordering DGX systems directly from NVIDIA, in addition to its existing OEM relationships. The exact ramifications for GPU procurement remain to be seen and have yet to be confirmed by management. But the inclusion of “DGX environments” in the partnership announcement is a meaningful tell, suggesting that at least some portion of future deployments (most likely at Sweetwater) will run on NVIDIA’s directly-sold turnkey systems rather than OEM-integrated alternatives.

It’s worth noting that DGX itself isn’t new. The product line has existed since 2016, spanning multiple chip generations from the original Pascal-based DGX-1 through to the current DGX B300 and the upcoming DGX VR200. What is new is the strategic emphasis NVIDIA is placing on DGX with the Rubin generation. DGX VR200 is being marketed as the ideal compute system for DSX-aligned facilities, with NVIDIA co-positioning the hardware and the data center architecture as a unified product offering rather than two separate purchases. This is a meaningful shift in posture. By pushing DGX harder as the default compute deployment inside DSX facilities, NVIDIA is effectively encouraging operators to bypass the OEM channel and procure directly from NVIDIA, allowing the company to capture more margin from each deployment that would otherwise have gone to Dell, Lenovo, or Supermicro. It’s a quiet but deliberate move up the value chain, consistent with NVIDIA’s broader pattern of extending control over more layers of the AI infrastructure stack.

Beyond the hardware itself, NVIDIA originally extended into managed cloud services via DGX Cloud, where NVIDIA contracted compute capacity from validated partner facilities and resold it to end customers as a managed cloud product. That product struggled to find adoption and was effectively wound down through 2025, with the team formally restructured in December 2025. NVIDIA has stepped back from competing directly with hyperscalers, and the DGX Cloud reseller model no longer exists as a customer-facing offering in any meaningful form.

NVIDIA’s broader cloud strategy has since evolved away from DGX Cloud toward a new platform called Lepton, which acts as a marketplace that connects compute customers directly with participating cloud providers. Instead of NVIDIA leasing capacity from neo-clouds and reselling it as their own product, Lepton functions more like an Airbnb model where NVIDIA facilitates the connection between providers and customers without sitting in the commercial chain itself. This sidesteps the friction with hyperscalers that ultimately killed DGX Cloud. The concept is genuinely interesting and could become a meaningful source of future revenue for IREN as Lepton matures, something I will likely explore in a future deep dive.

Why IREN Is NVIDIA’s Strategic Bet

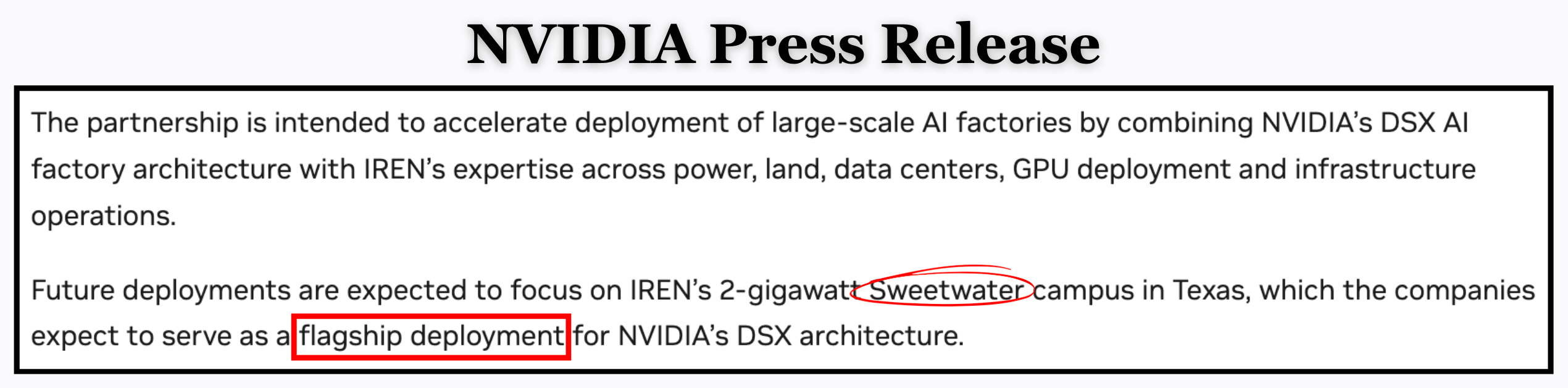

The combination of DSX and DGX deployments at IREN is what makes this partnership unique. DSX defines the facility architecture, DGX defines the compute systems deployed inside it. Looking at the public material published by both IREN and NVIDIA, it’s clear that IREN is being positioned as an important brand ambassador of both ecosystems. And with that, IREN’s massive Sweetwater campus will be the first full showcase of NVIDIA’s new Vera Rubin product lineup and DSX architecture systems. The companies explicitly position the 2 GW campus as a “flagship deployment for NVIDIA’s DSX architecture”.

The value proposition for NVIDIA is clear. The campus consists of two sites being connected by a direct fiber loop to form one homogenous data center campus, Sweetwater 1 (1.4 GW, recently energized) and Sweetwater 2 (600 MW, energization targeted late 2027). Both sites have all the necessary grid approvals in place, which positions Sweetwater as the single largest grid-connected data center campus in the world. That makes it a true unicorn project with substantial delivery certainty.

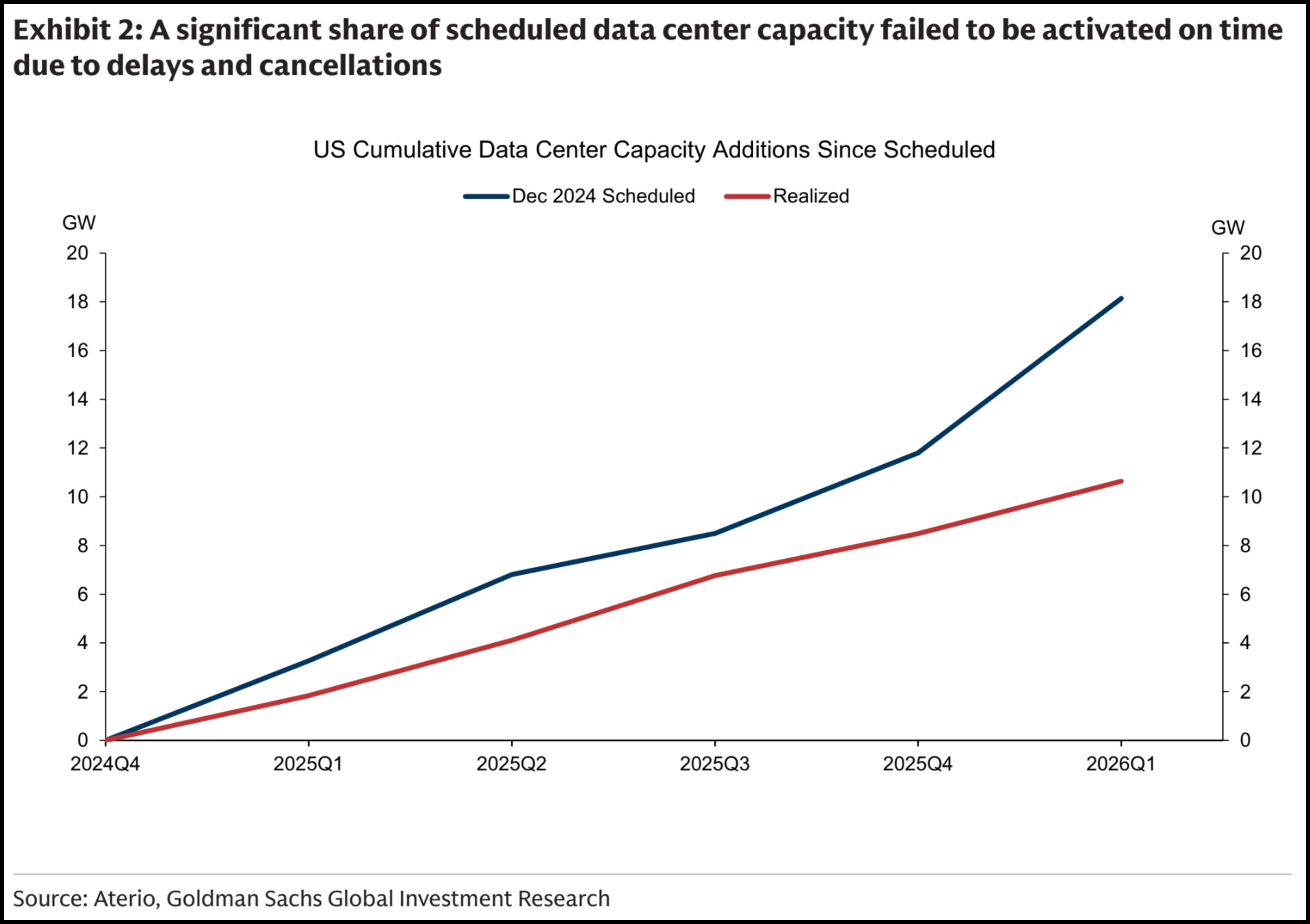

To appreciate why delivery certainty matters so much to NVIDIA, you need to understand what’s happening to data center development more broadly. As you may have heard, up to 50% of US data center projects slated for 2026 are being either delayed or outright cancelled, in large part due to power constraints. Goldman Sachs recently published data showing that of the ~18 GW of new data center capacity targeted for completion since Q4 2024, only about 11 GW actually got built.

Worse still, the rate of new data center completions has actually decreased over the past two quarters. This is a major problem for NVIDIA. As a hardware designer, NVIDIA’s sales are inherently tied to new data center infrastructure being built. After all, you wouldn’t be buying new GPUs today if your data center project is being delayed by a year.

On top of the supply-side challenges, cracks are starting to emerge in NVIDIA's market share dominance. Google with TPUs, Amazon with Trainium and Inferentia, Microsoft with Maia, and Meta with their MTIA chip. These aren’t just being developed for the hyperscalers’ own internal workloads anymore, but are now being offloaded to large-scale AI labs as well, directly taking market share from NVIDIA. Anthropic has been the poster child of diversifying its compute exposure, with its recent multi-billion dollar deals to consume Google TPU and Amazon Trainium capacity. To be fair, in these arrangements Anthropic isn’t directly purchasing custom silicon. They’re leasing cloud capacity from Google and AWS that runs on the hyperscalers’ dedicated chips. But for NVIDIA, that distinction doesn’t make a difference. The end result is the same. Hyperscalers are diversifying their hardware stack and to some extent are now actively competing with NVIDIA for new deployments.

So with new data center supply hitting severe roadblocks, coming online slower than anticipated, and hyperscalers taking more share of that limited supply, NVIDIA has to make very prudent decisions today so it ends up as the “Apple” of data center infrastructure rather than the “Cisco” of the dot-com era.

For one, NVIDIA is broadening its product portfolio well beyond just GPUs. DGX systems, DSX, Spectrum-X networking, BlueField DPUs, AI Enterprise software, NIM microservices, and the Omniverse digital twin ecosystem are all part of that broader push up the stack. While this expansion broadens revenue streams, it doesn’t directly address the threat that hyperscalers pose to NVIDIA’s core customer base.

For that, the primary step NVIDIA seems to have taken is to partner with the biggest neo-clouds, CoreWeave, Nebius, and now IREN, effectively diversifying its customer demand away from concentration in the hyperscalers. With the first two, NVIDIA has directly invested capital into the companies in exchange for promising “priority access” to new GPU iterations. However, I’d argue that the most important of these three partnerships has now been formed with IREN.

Out of the three neo-clouds, IREN is the only cloud provider that develops 100% of its data center facilities in-house. In essence, IREN has maximum control of its data center footprint and can therefore customize it to the fullest degree. Layered on top is the fact that IREN has by far the largest secured power portfolio of any neo-cloud, even rivaling those of hyperscalers. And keep in mind, IREN’s secured power is ramping at unprecedented speeds. At the start of this year it stood at 2.9 GW. Today, just five months later, it’s already at 5 GW.

These factors position IREN as the ideal partner for NVIDIA. The combination of secured power and full vertical control of the development process increases delivery certainty for large-scale data center deployments, something that’s not easy to come by in today’s environment. Moreover, it means that IREN is among the only viable options that can deploy NVIDIA’s full DSX-aligned ecosystem at gigawatt scale.

IREN has full control over facility design, architecture, supply chain, labor, and everything else needed to build a data center from the ground up, which means they can implement the DSX architecture to the highest degree. This essentially gives NVIDIA a clean canvas to showcase its DSX and DGX systems in the best way possible, positioning Sweetwater as a massive proof of concept for the world to see. Through the IREN partnership, Sweetwater is now unequivocally part of NVIDIA’s sales strategy and broader brand ecosystem.

NVIDIA’s Hidden Hand in the Mirantis Acquisition

A few days before IREN announced the NVIDIA partnership, the company disclosed the acquisition of Mirantis, a 650-person enterprise software company based in Campbell, California. On the surface, the acquisition reads as a logical move to strengthen IREN’s software stack. Mirantis brings AI infrastructure orchestration, multi-tenant cloud management, and over a decade of enterprise customer support experience. All of that is real, and it’s the version of the story IREN’s investor materials lead with.

But the timing, the strategic fit, and the deeper structural details point to something more interesting. There’s a strong case to be made that NVIDIA didn’t just bless this acquisition; they orchestrated it. The Mirantis transaction was likely a critical piece of NVIDIA's broader plan to position IREN as the flagship operator of its DSX rollout. And once you see the pieces fit together, the $3.4 billion AI Cloud contract starts looking less like a standard procurement deal and more like a structured onboarding program designed to bring IREN and Mirantis up to NVIDIA’s quality standards before Sweetwater goes live.

This is a non-consensus read of what just happened, and the public narrative hasn’t caught up to it yet. Let me walk you through the evidence that makes this theory not just plausible, but overwhelmingly likely to be true.