NUAI: A New Era of Compute

The bull case, the risks, and why this could be a massive re-rating story

Few data center developers have drawn as much attention from retail investors over the past several months as New Era Energy & Digital, the Permian-basin company listed on the Nasdaq under the ticker NUAI, and the reason is not hard to see.

At roughly $480 million in market value, with a project planned to scale toward 1.4 gigawatts, the asymmetry on offer is the kind that rarely comes along. For now, though, most of that remains a plan. NUAI has spent the past year laying out what it intends to build, and has yet to prove it can actually deliver.

The market has not made up its mind about any of it. To the skeptics, NUAI is a company with almost no operating history. To the believers, it is a genuine mispricing the wider world has not caught up to yet.

The bulls are betting on the strategy, which is one of the most differentiated in the entire data center and colocation industry. It is built around the one variable that now decides who gets to build, which is access to power. Most of the companies chasing that prize are giants stuck in the same congested grid queues as everyone else. NUAI is coming at it from a different direction, with a model for power, land, and capital that almost none of its listed peers are attempting at this scale. Executed close to the way management intends, that head start could translate into serious upside for shareholders. The reward for being early and right in a business like this tends to come in multiples rather than percentage points.

Whether that upside is real, or whether the doubters have it right, is exactly what I set out to answer. In this deep dive I break down the thesis in full, where NUAI genuinely has an edge and where the shortcomings and the risks lie. At the end of the report we’ll determine whether this is a name worth following closely, and ultimately one worth holding over the long term.

Enjoy!

The Behind-the-Meter Shift

Until recently, almost every data center in the country ran on the same assumption, that its power would come from the grid. A developer secured a site, applied to the local utility or grid operator, and worked through a fairly standard sequence to get connected. There were studies to gauge what a large new load would do to the surrounding network, an interconnection agreement to sign, and in some cases substations or transmission lines to build or upgrade. None of it was glamorous, but in the years before artificial intelligence reshaped demand, getting connected was rarely the thing that held a project up. A typical site could often go from planned to powered in under two years, and grid power was simply the default, cheap, reliable, and usually there when you needed it.

The companies that now build and lease out large AI-ready data centers arrived in the business from an unlikely starting point. Most of the listed names that dominate this corner of the market came out of bitcoin mining, including Core Scientific, Applied Digital, TeraWulf, Hut 8, and Cipher Mining. They built their footprints when securing large blocks of electricity was still relatively easy, and that timing turned out to matter enormously.

For most of the internet’s history, data centers clustered around a handful of dense network hubs, places like Silicon Valley, Dallas, Chicago, and the New York and New Jersey corridor, where they could sit close to users and to the fiber that carried their traffic. The largest cluster of all formed in Northern Virginia, which is not a major population center in the way the others are, but which became the busiest data center market on earth because a huge share of the world’s internet traffic physically routes through it. Bitcoin miners never needed any of that. Latency and proximity to users were irrelevant to them, so they were free to chase the one thing they did care about, which was cheap and abundant power, into remote parts of the country where it was plentiful. That freedom let them assemble power portfolios measured in hundreds of megawatts, and in some cases gigawatts, with relative ease.

Then artificial intelligence arrived, and the demand curve for computing power bent sharply upward. Almost overnight, the binding constraint on building a new data center stopped being just land or capital and became electricity. As every developer in the industry rushed to lock down grid-connected power at the same time, the queues to interconnect stretched out, and in the most congested markets the wait for a large new connection now runs as long as seven years. The only thing that brings those timelines back down is a return to balance between supply and demand, which in practice means new electricity generation being added to the grid at roughly the pace new demand arrives. Adding that supply is a slow process with hard physical limits, since power plants and transmission lines take years to permit and build. It is entirely plausible that the imbalance persists well into the next decade before it eases.

That backdrop handed a quiet but powerful advantage to anyone who had secured power early, or who had at least started the multi-year process of securing it well ahead of the crowd. Bitcoin miners largely belonged to that group, and they are collecting the reward now. Many of their operating mining sites, along with empty parcels they had already connected to the grid for future mining expansion, are being converted into large-scale data center campuses and leased to hyperscalers and large neocloud operators. This kind of arrangement, where a developer builds and powers the facility and a tenant moves its computing in, is what the industry calls colocation, and it has created a great deal of value for the former miners that pivoted into it. The catch is that their available power is running down, and the same is true across the rest of the industry.

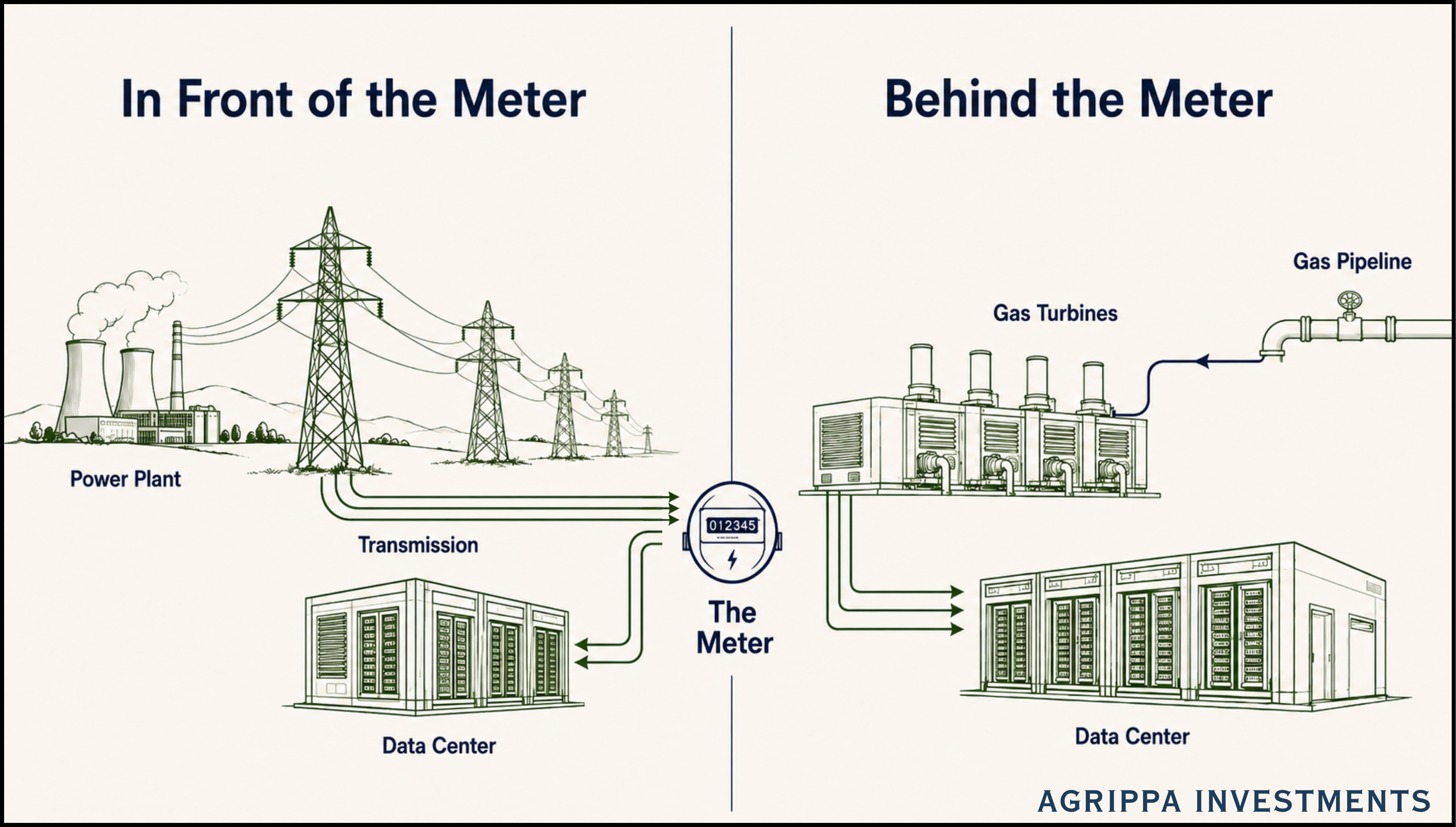

Grid-connected power remains one of the hottest commodities in the sector, but the industry is adapting to the shortage in real time, and the main way it is doing so is by going around the grid altogether. That approach is what the industry calls behind-the-meter, or BTM, and the name is close to literal once you picture the meter itself.

The meter is simply the boundary between two sides. In front of it sits the public grid, the power plants and transmission lines that produce electricity somewhere far away and send it to you across the network, with the utility measuring and billing every unit that crosses over. Behind it sits your own property and whatever you choose to put on it. In its purest form, a behind-the-meter project places its own generation on that near side, right next to the load it serves, so the power is produced and consumed in the same place rather than pulled in from the grid. There is more than one way to do this, but the most common is to generate the power on the data center campus itself, almost always with natural gas. Gas is cheap where it is plentiful and can run steadily around the clock in a way that wind or solar cannot, which makes it the natural fuel for a data center that can never go dark. The electricity itself comes from turbines or engines burning the gas, fed by a pipeline running into the campus.

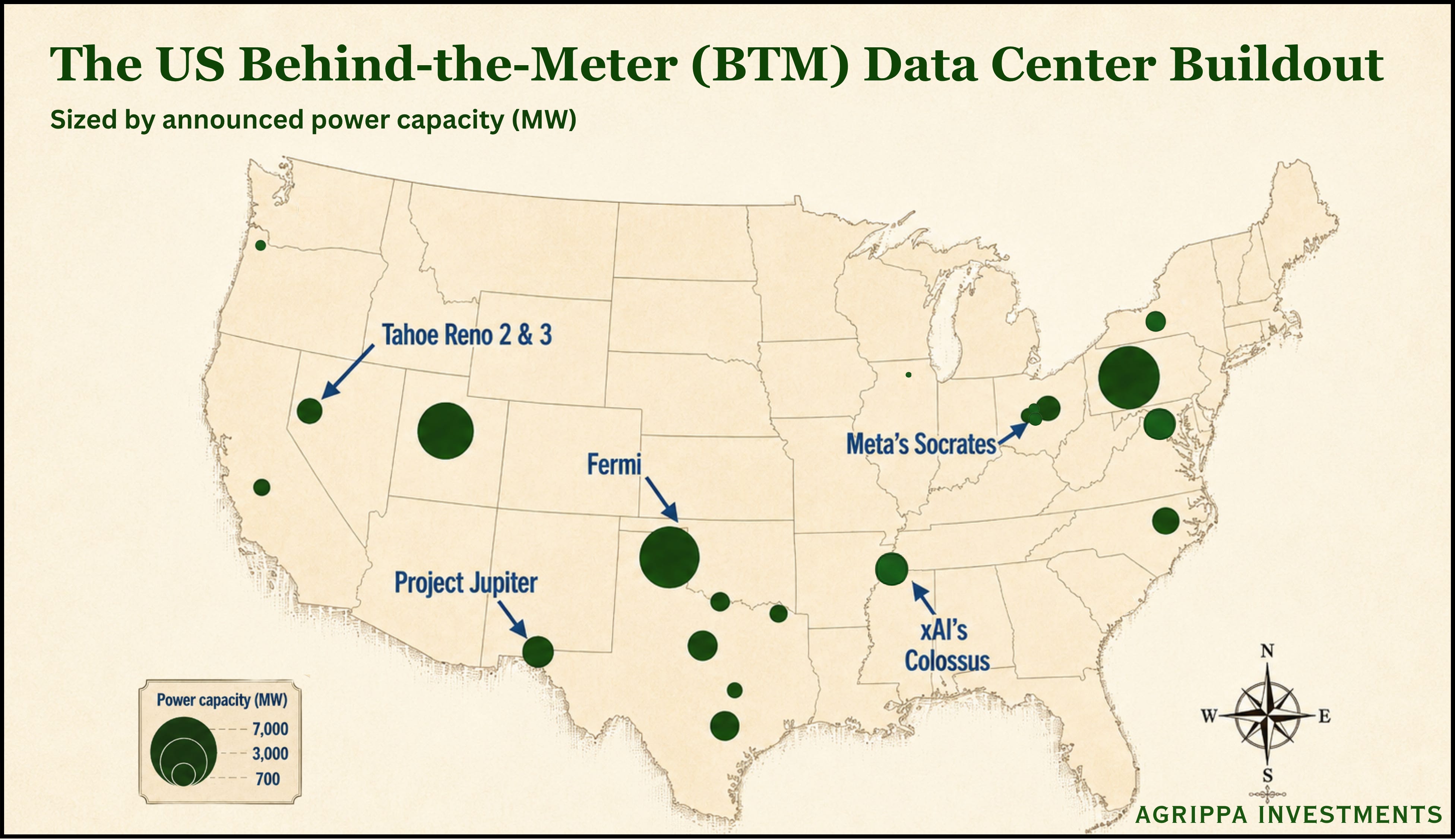

The shift towards BTM is spreading quickly, and not only among the smaller players. Some of the colocation companies that built their businesses on grid connectivity are now pivoting toward generating their own power, Cipher Mining among them, as the supply of readily available grid-connected sites thins out and its leadership steers it toward behind-the-meter development. The trend runs all the way up to the largest projects in the country. Several of the biggest hyperscale campuses now under construction are being built behind the meter, including xAI’s Colossus in Memphis, Oracle’s Project Jupiter, and Meta’s Socrates site, among others.

There is a political tailwind behind all of this as well. The current US administration has been openly concerned about AI data centers straining the grid and pushing up electricity bills for ordinary households, and it has encouraged the idea that very large power users should bring their own generation rather than lean on public grids. In practice that support is more rhetorical than legislative, with little binding policy behind it, and I would not lean on it as a real driver. What it does provide, however, is cover. It lets a hyperscaler commit billions of dollars to burning natural gas on site and present the decision as a way of sparing nearby residents from higher electricity prices, rather than as the heavily polluting choice it might otherwise appear to be.

None of this means behind-the-meter is easy, and there is a reason grid power remains the preferred option for anyone who could have both. A grid connection, for all its waiting times, is fundamentally simple to operate, because the utility provider handles the generation and the reliability. A behind-the-meter project has to do all of that itself. Producing your own power at this scale is a power plant operator’s job, and it sits well outside the skill set most data center developers were built around. The site itself also has to be right. On-site generation almost always means burning natural gas, so the campus needs direct access to a gas supply, and ideally to more than one pipeline, since a single line is a single point of failure that could take the whole site offline if anything happens to it. On top of that, a gas plant running around the clock is loud and produces real air pollution, which makes these projects a hard sell anywhere near where people live and rules out a lot of the places a developer might otherwise want to build.

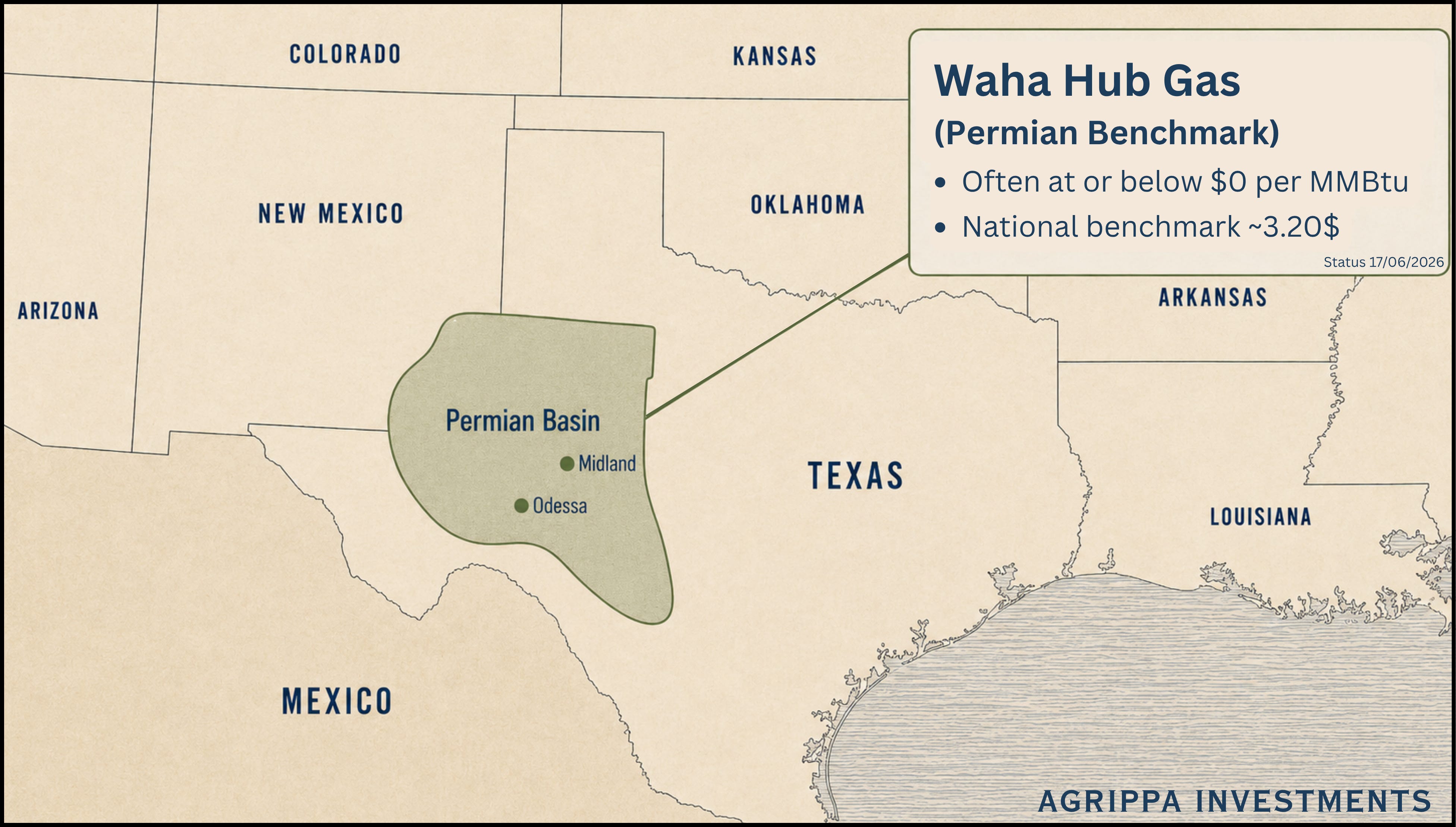

These operational headaches and geographic requirements are precisely the kind of problems that open the door for a company like NUAI. New Era began as a small Permian natural gas and helium business, and the people running it built their careers in oil and gas. The company’s sites sit in the Permian Basin, the stretch of West Texas and southeastern New Mexico that has grown over the past few decades into one of the largest oil and gas producing regions in the world.

For a behind-the-meter strategy, you could hardly ask for better ground. Gas here is so abundant that it frequently costs nothing at all. The Permian is an oil basin first, and much of its gas comes up as a byproduct of the crude, in such volumes that the pipelines out of the region cannot carry it all, which pushes the local price to or below zero and leaves producers paying to offload what they cannot move. The fuel still has to be processed and piped to wherever it is used, so nobody truly runs on free gas, but as a starting input it is about as cheap as energy gets anywhere.

Moreover, it goes without saying that the region has ample gas infrastructure, including a robust network of pipelines running across it. This ticks yet another important box for any data center developer looking to pursue a BTM strategy here. And because the Permian is both thinly populated and thoroughly industrial, the noise and air pollution that come with running gas turbines around the clock barely register. This is a region dotted with wells, pipelines, and processing plants, so the people who do live here are long used to that kind of activity, and the communities nearby are more likely to welcome the jobs and economic activity a large data center campus brings than to fight it.

There is one more feature of the Permian that’s worth pointing out, and it has nothing to do with geology. In business terms, the region is fairly closed to outsiders. Many of the operators that run it are private, relationship-driven companies that have worked the same ground for decades, and a great deal of business there gets done through long-standing personal networks and trust, where a cold introduction counts for very little. Some of that is simply how a tight-knit industry in a remote place tends to operate, and some of it is a genuine wariness of newcomers, particularly technology outsiders seen as arriving to do whatever they like on someone else’s turf. For an operator with no local standing, that culture is a real obstacle.

NUAI does not have that problem. Its roots are in the Permian, and its senior management came out of the region’s energy industry. That opens doors a Silicon Valley developer parachuting in would find shut, and it makes NUAI a natural local partner, the kind a hyperscaler can work through to navigate the basin without having to earn that trust on its own.

Put it together and the setup starts to make sense. The industry’s central bottleneck is power, and the workaround is to generate it on site. The hard parts of doing that are finding cheap fuel, building real pipeline redundancy, staying clear of communities that fight these projects, and earning the trust of a region that does not hand it out easily. The Permian answers the first three almost by default, and NUAI’s origins go a long way toward the fourth. Whether the company can actually turn those advantages into a signed, financed, operating campus is a separate question, and the one the rest of this report is built to answer.

NUAI Overview

New Era Energy & Digital is a young company wearing a new name. It trades on the Nasdaq as NUAI, but for most of its short public life it was New Era Helium, a small Permian natural gas and helium producer that became public through a SPAC merger at the end of 2024. The person behind it is E. Will Gray II, who built the company and ran it as chairman and chief executive through most of its public life, and a West Texas energy man. As of July 2026 he has handed the chief executive role to Charlie Nelson, the company’s former COO, and moved into a new position leading the company’s Permian Basin efforts.